Bitcoin Still Diversifies Portfolios Despite Tech Stock Moves

NYDIG says Bitcoin still diversifies portfolios in March 2026 despite rising S&P 500 and Nasdaq correlation — three-quarters of BTC moves stay crypto-driven.

What to Know

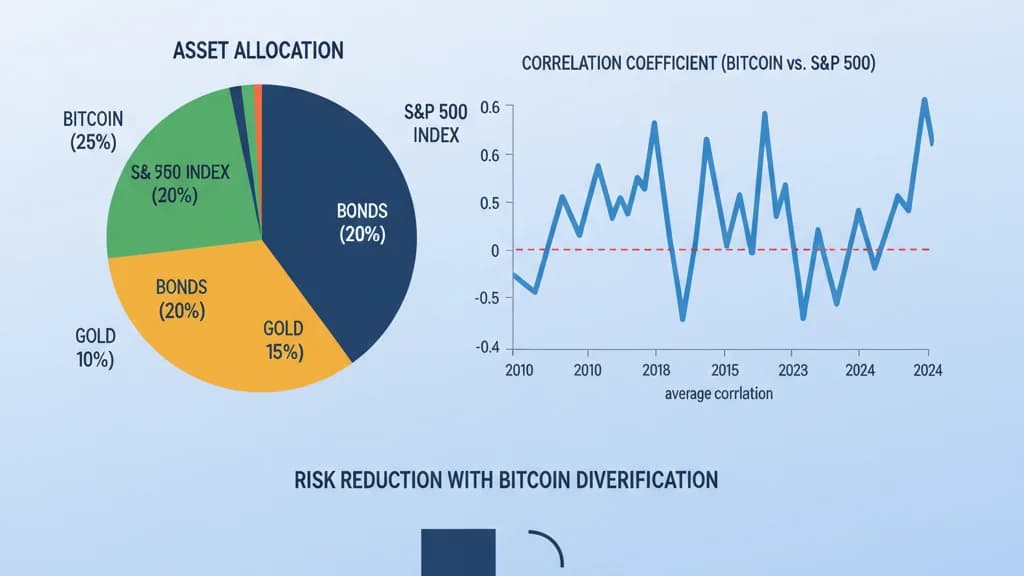

- NYDIG research head Greg Cipolaro argues Bitcoin's correlation with equities near 0.5 still leaves roughly three-quarters of BTC price moves driven by crypto-specific forces

- Chamath Palihapitiya and Ray Dalio have questioned Bitcoin's suitability as a central bank reserve asset, but NYDIG says sovereign adoption is not required for continued growth

- Cipolaro attributes recent Bitcoin-equity alignment to the current macro backdrop — shared sensitivity to liquidity conditions — not a structural merger of asset classes

Bitcoin portfolio diversification still holds up — that's the blunt conclusion from NYDIG this Sunday. Even as BTC has moved in closer lockstep with U.S. equities, the firm's global head of research Greg Cipolaro published a weekly market note pushing back hard against the narrative that bitcoin is now just a high-beta tech trade.

The Correlation Math Everyone Is Getting Wrong

Yes, correlations between bitcoin and benchmarks like the S&P 500, the Nasdaq 100, and the software-heavy IGV ETF have climbed in recent months. Cipolaro acknowledged that plainly. But here's where most of the analysis you're seeing online falls apart.

A correlation of 0.5 sounds decisive. In practice, it means equity markets explain roughly one-quarter of bitcoin's price moves. The remaining three-quarters of BTC's daily action is driven by forces that have nothing to do with stocks — Bitcoin fund flows, shifts in derivatives positioning, network adoption data, and regulatory developments. That's not a proxy for Nvidia.

Cipolaro puts it plainly: cross-asset correlations being elevated is not the same as those correlations being determinative. The former says BTC sometimes moves with equities. The latter would mean equities explain BTC. Right now, they don't.

While cross-asset correlations with equities are currently elevated, they remain far from determinative of bitcoin's returns.

Why Is Bitcoin Moving With Tech Stocks Right Now?

Macro. Both bitcoin and growth stocks respond to the same liquidity environment and the same risk appetite swings. When the Fed tightens, both sell off. That's not structural convergence — it's two assets sitting in the same macro current.

According to NYDIG, that shared macro sensitivity is precisely what supports bitcoin's diversification case rather than undermining it. The note frames recent price alignment as a cyclical feature of the current environment, not evidence that bitcoin has permanently transformed into an equity surrogate. Oil and gold respond to liquidity cycles too. Nobody calls crude a tech stock.

Dalio and Palihapitiya Versus the Bitcoin Bulls

Cipolaro's note addressed the larger debate head-on. Both Chamath Palihapitiya and Ray Dalio have raised doubts about whether BTC can serve as a reserve asset on sovereign balance sheets — and the crypto community has taken notice.

Palihapitiya, who called bitcoin "Gold 2.0" back in 2013, has since questioned whether the asset fits the structural needs of central banks. Dalio's criticisms are longstanding: volatility, regulatory risk, and technological threats including quantum computing. Cipolaro's read? These aren't early believers going bearish. They reflect a shift in the debate itself — from whether bitcoin survives to whether it can become a central bank reserve asset. That's a much harder bar, and asking it signals how far the asset has already traveled.

Does Bitcoin Actually Need Central Banks?

Cipolaro's answer is no — and it's worth taking seriously. Bitcoin's adoption path has run opposite to most financial innovations, which typically start with institutional capital and filter to retail. BTC started with individuals, then family offices, asset managers, and now ETFs drawing in broad retail flows all over again.

Central bank adoption would validate the asset class, he acknowledged. But it is not a prerequisite for continued growth. What matters is the network itself: global distribution, political neutrality, censorship-resistant value transfer, digital scarcity, and independence from any single government or monetary authority.

Sovereign balance sheets may eventually get there. Or they may not. Either way, the capital keeps coming.

Central bank ownership may ultimately validate the asset class further, but it is not a prerequisite for continued growth.